In this piece our policy team analyse the recent R&D statistics released by the ONS. In a future piece we will look at the implications of these new statistics for policy and advocacy by the sector.

The Office for National Statistics (ONS) have published the latest figures for R&D expenditure in the UK in 2020 (GERD). The ONS have made significant changes to the methodology used to estimate R&D performed by businesses and the higher education sector. As a result of using the revised methodology the ONS has found that there is substantially more R&D in the UK economy than previously captured by official statistics.

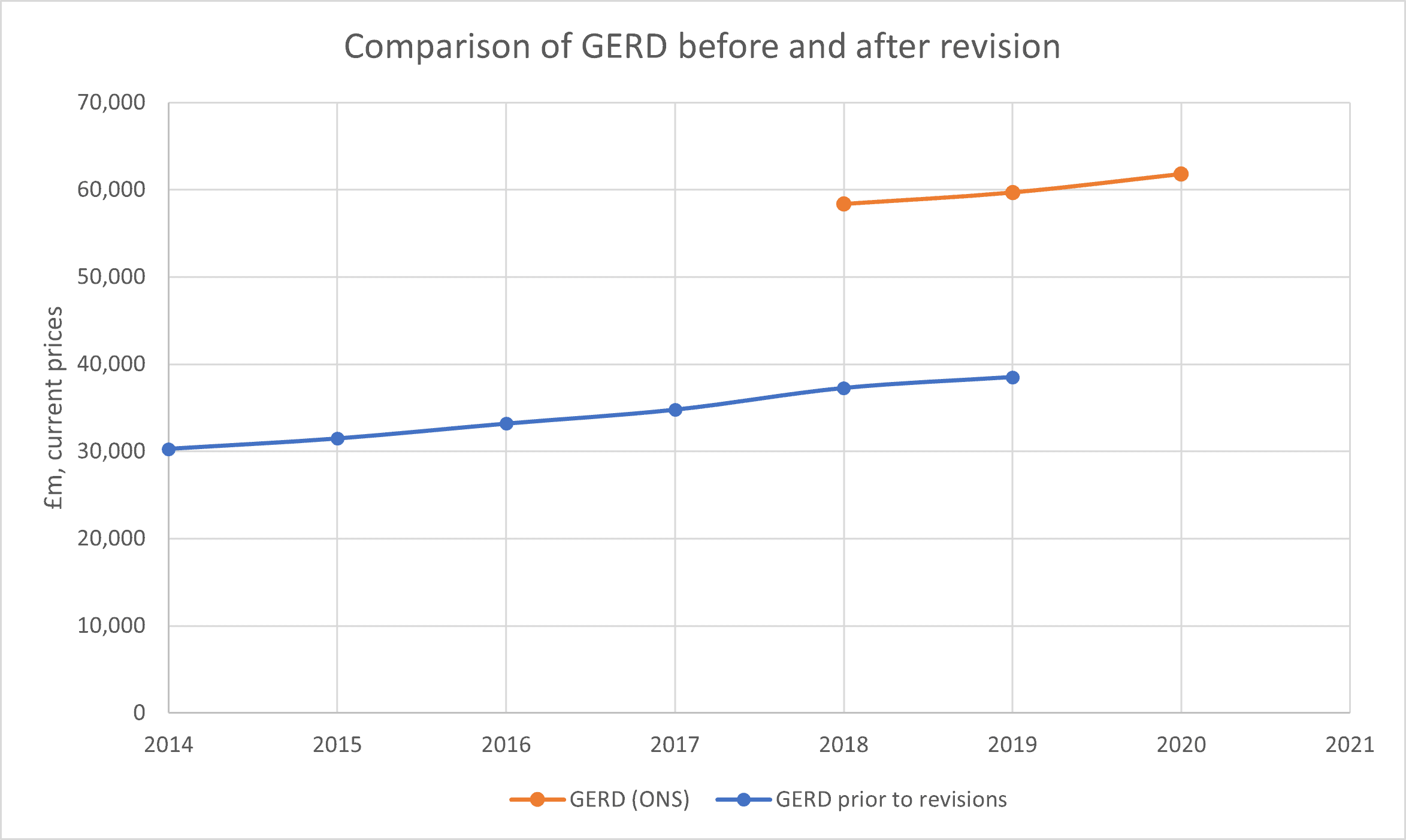

The new GERD release only backdates the new methodology to 2018, meaning longer term comparisons are no longer possible. The data shows that in 2020 the UK invested £61.8 bn in R&D. The figures for 2019 and 2018 are £59.7bn, and £58.4bn, respectively. This represents a substantial change in the level of R&D in the UK economy than previous estimates showed. Last year’s GERD release, before the methodology was updated, showed R&D expenditure at £38.5bn in 2019. The graph below shows just how large this change is.

Where is this extra R&D?

The big change from previous statistics is that there is much higher expenditure by businesses on R&D than previously thought, as we discussed when the ONS published its revised methodology. In previous BERD statistics there was an under-representation of smaller businesses, and so the ONS updated the methodology used to better represent R&D conducted by smaller businesses in the statistics. The latest BERD release shows that in 2021, businesses invested £46.9bn in R&D. In 2018, 2019 and 2020 businesses invested £41bn, £42bn and £44bn, respectively. This is £15.8bn, £16.1bn, and £17.1bn higher than previously published, before the methodology was updated.

There has also been a change to how R&D performance in the higher education sector is measured. The ONS have introduced a new data source, the Transparent Approach to Costing (TRAC). This method aims to better capture R&D that is both performed and funded from within the sector itself (for example funded by surpluses from other activities not directly related to R&D), which previously did not appear in the statistics. In 2020, these changes have resulted in a new estimate of R&D funded from within the sector itself of £4.9bn in 2020. Therefore, estimates of R&D performed by the higher education sector have been revised, from £8.7bn to £14bn in 2018 and from £9.1bn to £14bn in 2019.

What does this all mean for the trends in R&D expenditure?

The changes to business and higher education R&D spending have been implemented from 2018 onwards. As the new baseline is 2018, it is not possible to make comparisons with previous releases and is difficult to comment on longer-term trends in R&D investment.

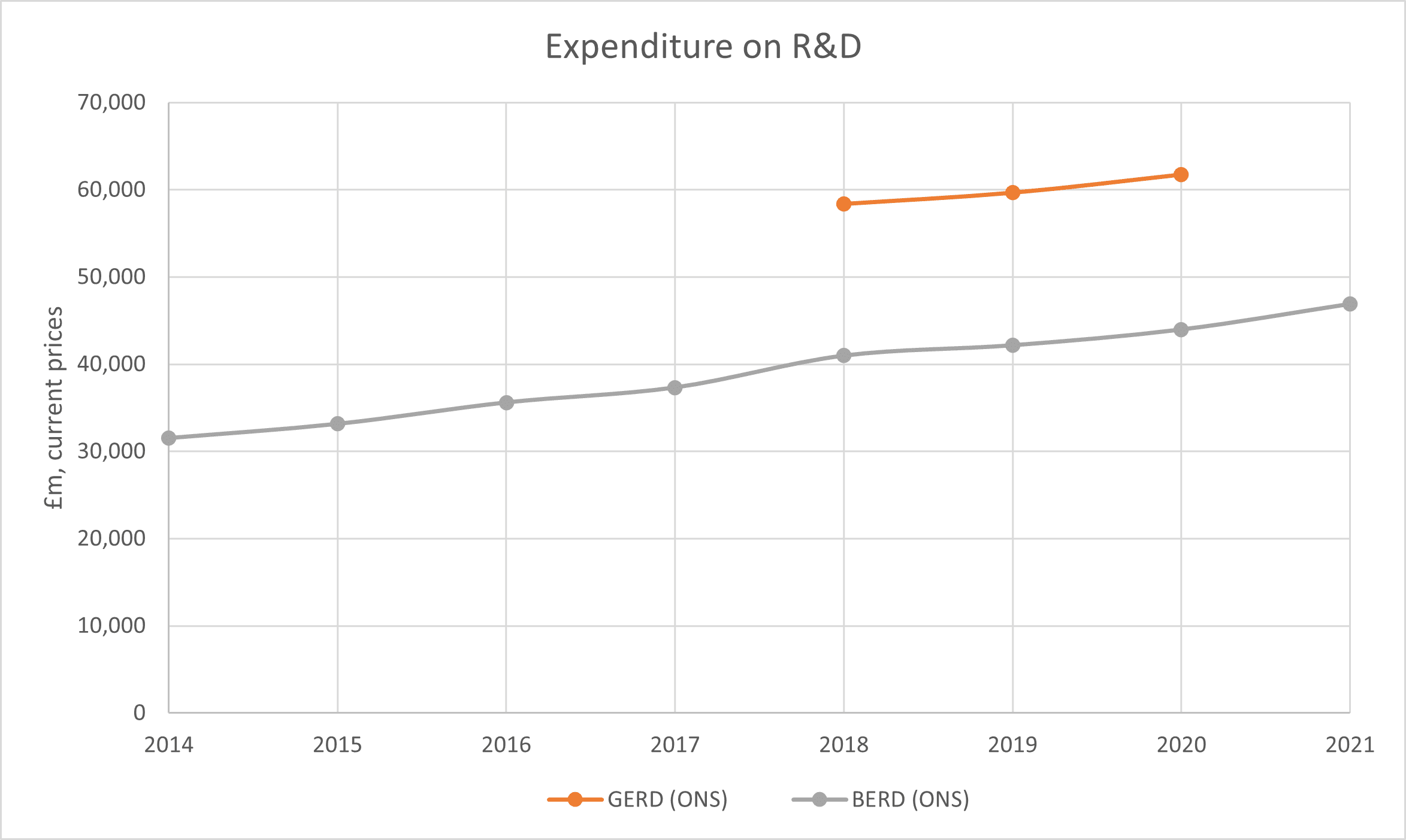

The graph below shows the total GERD figures for 2018, 2019, 2020 (orange line) using the new methodology and the total BERD figures 2014-2021 (grey line), using the new methodology for business investment. While we do not have a back-dated trend for the GERD figures, the second graph shows that business comprises a very substantial proportion of the total and therefore the trend increase in BERD is likely to have been replicated in GERD over the same time frame.

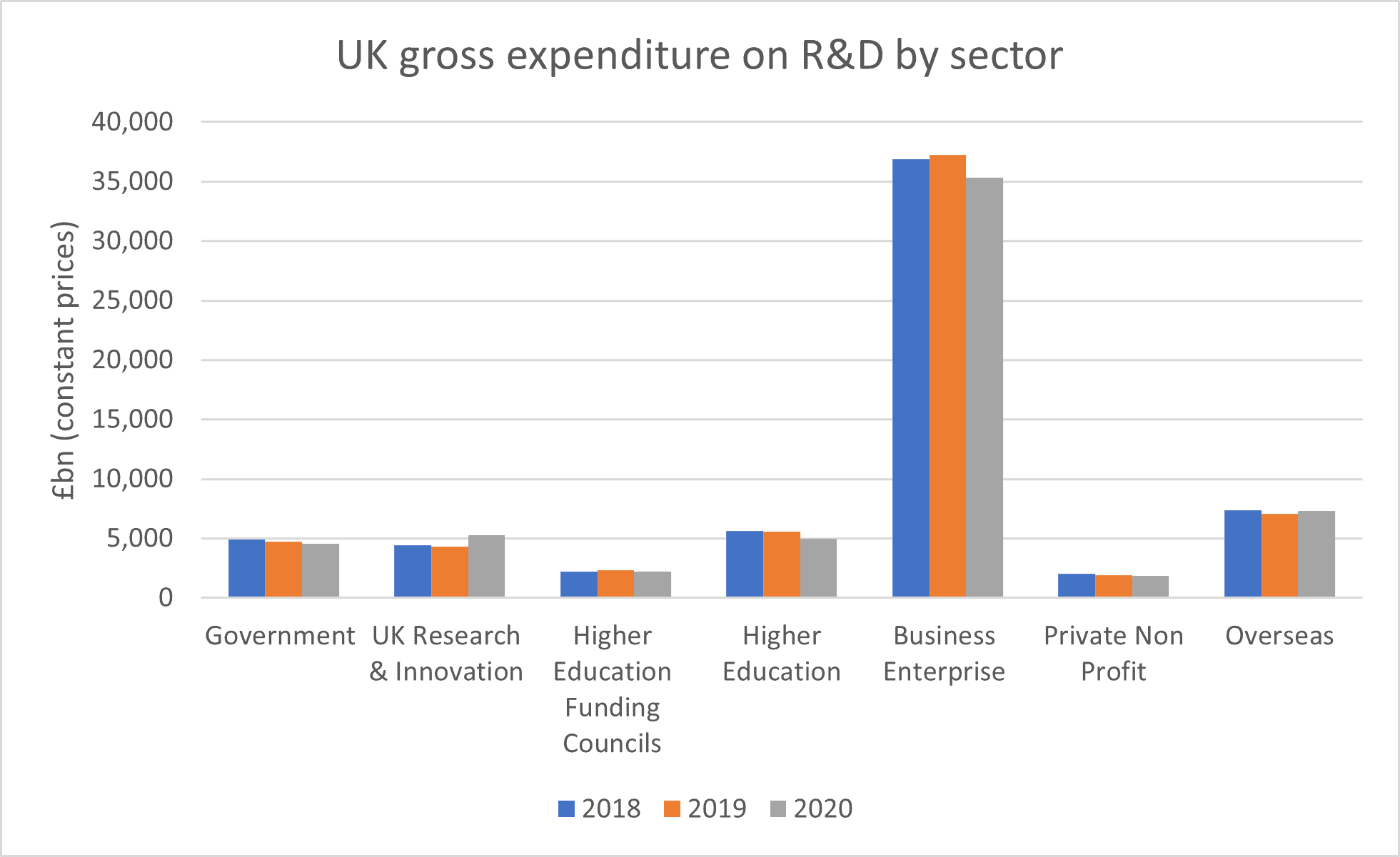

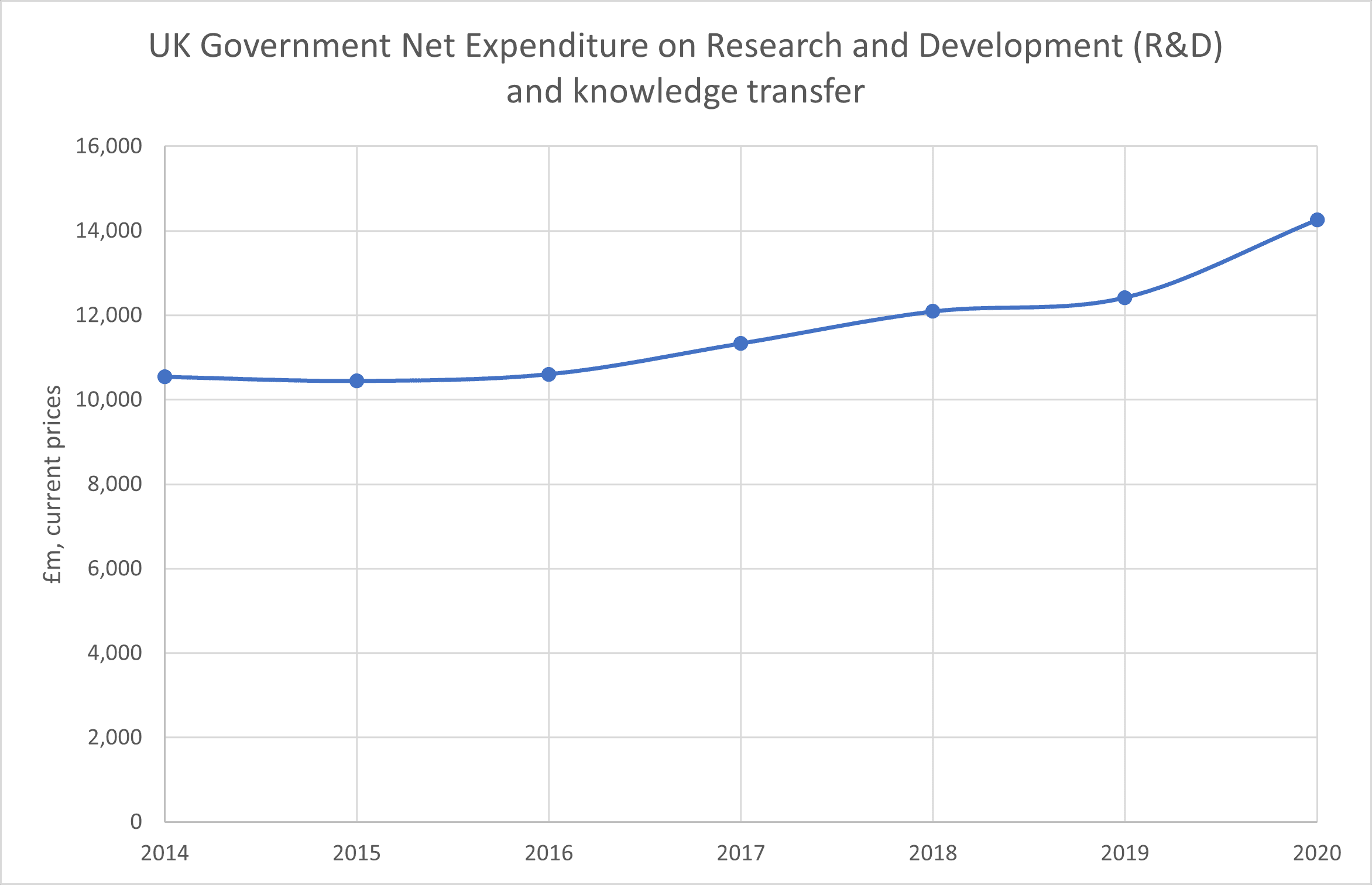

If we look ‘under the bonnet’ a little at Government spending we do see a substantial UKRI uplift in 2020 and this is also reflected in the third graph. The third graph shows GovERD statistics from earlier in the year. Government expenditure was broadly flat 2014-2016 then started to increase slowly from 2016 before a bigger jump in 2020.

A couple of other things to note

While in cash terms R&D investment has increased across 2018, 2019 and 2020 in virtually all sectors, inflation is already starting to bite, with investment in R&D staying relatively flat between 2018 and 2020 in constant 2021 prices.

There was also a decrease in many sectors in 2020. The slight drop in 2020 could reflect the temporary impact of the COVID-19 pandemic. We can see from the BERD statistics that are available up to 2021 that the increase picked up again in 2021. For the other areas we will have to wait for next year’s release.

What are the implications for research intensity and what does it all mean?

As we have previously commented, the new estimates for business R&D have important implications for the gross domestic expenditure on R&D (GERD) results, and hence the level of research intensity in the UK. As an initial back of the envelope calculation we have revisited our projections to update our model with these new figures. Our rough estimate is that the UK invested 2.7% of GDP in R&D in 2018. Because the revisions don’t go back further, we are not able to calculate when the UK reached the Government’s target of 2.4% of GDP in R&D. These initial estimates however should be interpreted with caution – the ONS themselves have not yet provided research intensity figures, as calculations of GDP will need to include the revised R&D statistics. The ONS have indicated that the earliest opportunity to add the revised R&D estimates into national accounts will likely be towards the end of 2023.

As the UK economy is more research intensive than thought, the UK has very likely already reached the Government’s 2.4% research intensity target, which is good news. However, the principles that underpinned that target still remain. We must continue to build on the current foundations and take the UK’s ambitions higher. It is great that the Government has moved to bolster its stance on research and innovation, placing it front and centre of its ambitions for growth. Stability of intent, supported by sustained investment, is vital to help research and innovation thrive in a way that improves people’s lives and livelihoods.

These statistical revisions are very large and are likely to have a significant and continued impact on the R&D policy space and discussions as we move forward. At CaSE, we are working through many of these implications and as an initial step we will be publishing a piece soon with our thoughts on some of the impact on policy and advocacy that these statistics will have.

Related resources

Significant cuts following STFC prioritisation

09 July 2026

UKRI have published ‘prioritisation’ at the STFC to bring down projected costs, the consequences will be significant cuts to some areas and facilities funded by the STFC.

Conservative Party plans highlight the shifting political landscape for UK R&D

30 April 2026

Conservative Party have presented a defence policy proposal that includes a reduction of UKRI funding by £2 billion per year. CaSE has looked at this proposal and what it indicates about the wider position of R&D in public policy.

Julia Lopez MP reply to CaSE letter on Conservative defence R&D plans

30 April 2026

CaSE has received a reply to our letter to the Conservative Shadow Secretary of State for Science, Innovation and Technology, Julia Lopez MP, which asked for clarity surrounding their policy position that would see a reduction of UKRI funding by £2 billion per year.

An update on UKRI’s funding changes

30 April 2026

A recap of the updates and discussions surrounding the new UKRI budget framework and a summary of the latest dialogue between UKRI and the House of Commons Science, Innovation and Technology Committee.